A Peek Into The World of Chargebacks

Transactions and money exchange through credit cards have proven to be very beneficial in online business. It aids in increasing revenue and your customer base, in addition with the improvement in overall productivity. All you have to do is- Get yourself a merchant account to be able to accept cards for payments. With this, you add convenience, cost-effectiveness and a professional image right into your business.

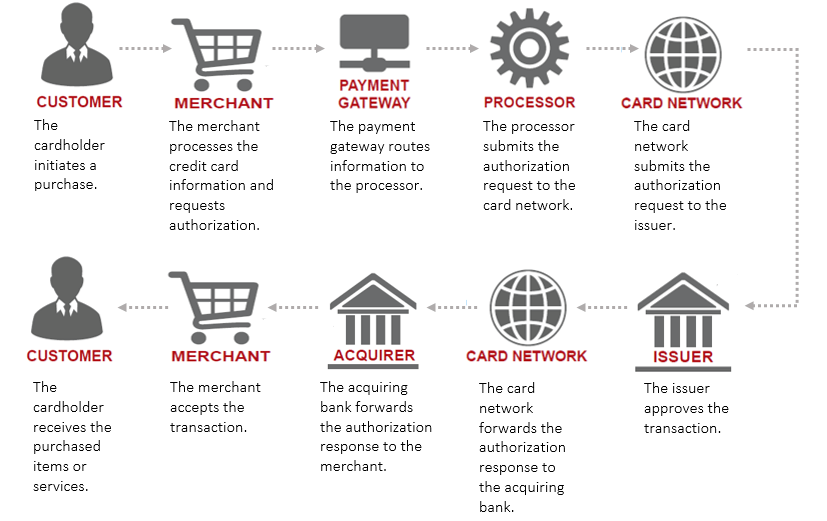

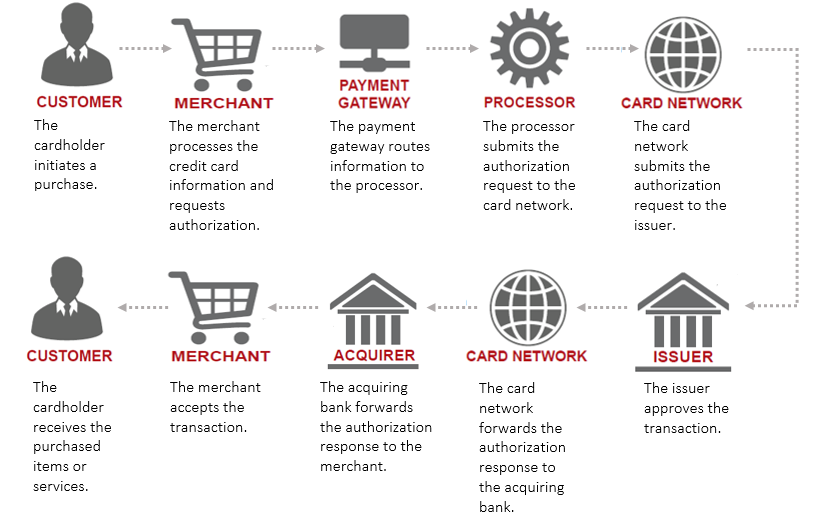

If you have already covered this step, you probably realize how confusing credit card processing can be. Here is a figure to simplify it for you.

Given that it may take time for you to get around with this entire process, there is one important aspect about merchant accounts that you need to know very well - chargebacks.

Whether you are someone who is just curious about how a chargeback works, or a seller who has received his first chargeback, it is important to understand how chargebacks have a great and irreversible impact on an online business.

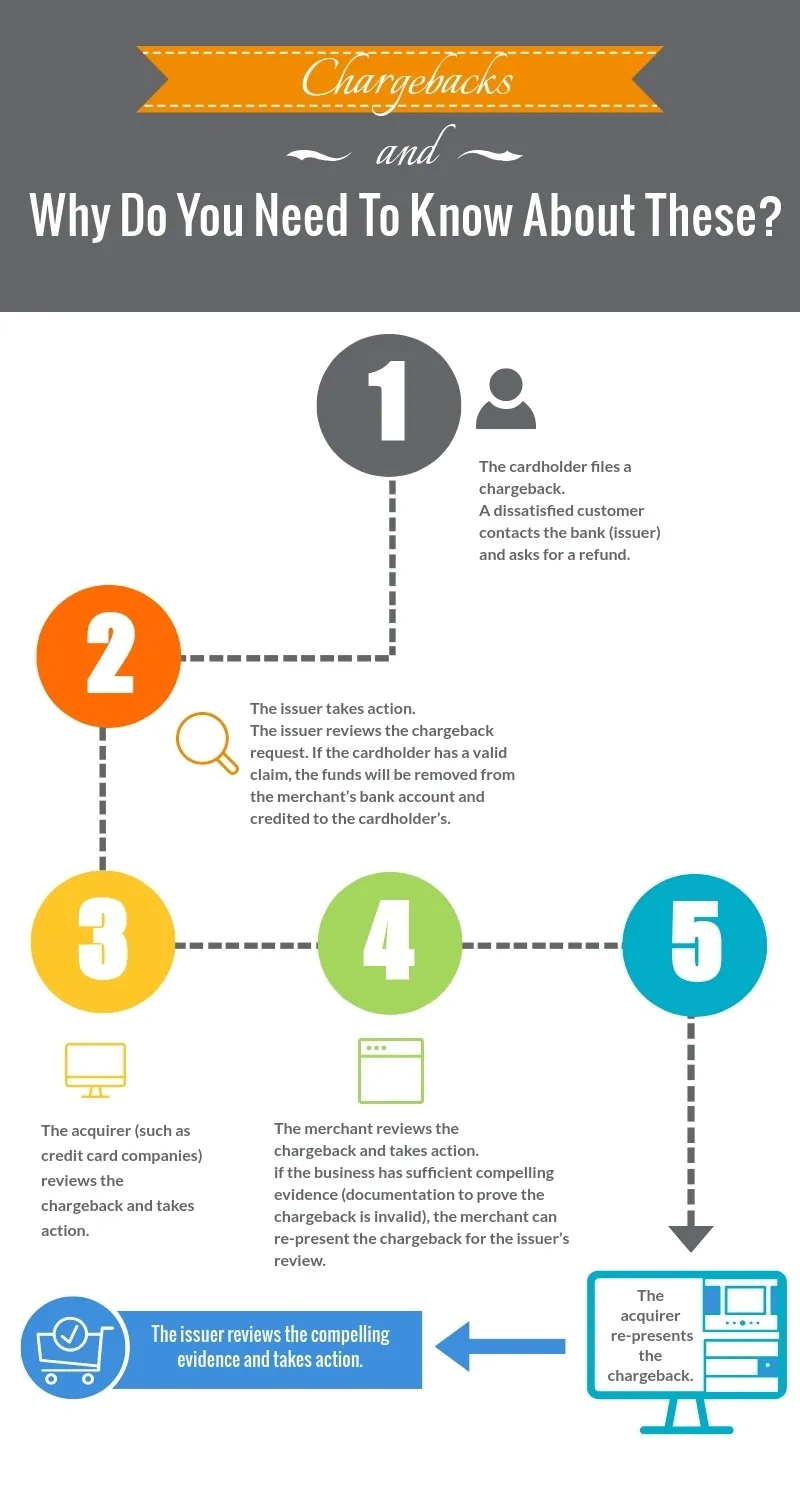

In chargeback process, cardholders file a dispute with their issuing bank, at which point the merchant’s bank is debited the amount of the transaction that was previously credited. The merchant must provide compelling evidence to disprove any fraudulent activity associated with the transaction. If the issuing bank deems the evidence enough to overturn the cardholder’s dispute, the funds are returned to the merchant. If the cardholder still believes he was the victim of fraud, he can initiate a second chargeback, also called pre-arbitration.

When Consumers Can Legally Use Chargebacks

It is undeniably important to understand when consumers can use the privilege of chargebacks.

In any case of identity theft and unauthorized transactions, the victim should contact the bank immediately. This is necessary not only to recoup victim’s stolen money, but also to help prevent future losses.

However, it is for the consumer’s betterment to contact the merchant directly when fraud has or seems to have occurred.

In some cases, it is observed that the supposed fraud was actually an accident. This could happen as an innocent under which the consumer has forgotten about the purchase. Additionally, a refund is recommended because it usually puts money back in the consumer’s account much quicker than a chargeback.

Filing a chargeback instead of seeking a traditional refund when unsatisfied with a purchase is cyber shoplifting.

Filing an illegitimate chargeback allows the cardholder to retain possession of the purchased item, even after the purchase amount has been refunded. Consumers need to request a traditional refund from the merchant and return the item, making it possible for the merchant to sell the merchandise again for a profit. Otherwise, the consumer is getting something for free—the very definition of stealing.

Types of Chargebacks

Chargebacks can be catergorized into three types.

1. Merchant Error

Merchant error chargeback is the most common type of chargebacks. Merchant side errors don’t necessarily mean to be intentional. But, the effects of such mistakes end up bringing a great deal of harm and damage to the store in different ways.

Following are some of the observed reasons of these chargebacks-

- System errors or problems arising from your business process

- Poor customer service

- Unwanted recurring payments

- Authorization errors or faulty product fulfillment.

Customers are liable to filing a chargeback if your system is generating their bills without their knowledge or consent. This type of recurring billing chargebacks is common with the businesses that accept payments in installments.

2. Unauthorized Card Use

This category deals with an actual fraud. Purchase made by an individual is completed by a presumably stolen credit card information while the legitimate card holder is unaware of the transaction made. So, the owner of the credit card is sure to file a chargeback. Such a transaction is illegal and laws in place can severely punish the person held responsible for this crime.

Occasionally, this chargeback can be a result of some internal misunderstading.

Sometimes, a family member could make a purchase using a family credit card and another member of their family may not be aware of that transaction and could file a claim against your business.

3. Friendly Fraud

This type of fraud is also considered to be an honest and innocent mistake. But this time, unlike from merchant’s side in ‘Merchant Error’ category, this is a mistake from consumer’s side.

A customer committing friendly fraud doesn’t present a potential threat to your business. You can assume this type of fraudster belongs to the confused, misguided or forgetful lot.

For subscription merchants, this usually manifests in customers who legitimately agreed to recurring billing, but were genuinely unaware of what they were agreeing to. No matter how many fail-safes and opt-ins your business uses, there will always be a customer who overlooks the terms of an agreement. That doesn’t mean the customer won’t be interested in your services in the future.

Banning this customer from making purchases at your store is not recommended. You should rather work to get to the roots of misunderstanding and this way, prevent such scenarios from occurring anytime in future.

Who all are involved in a Chargeback?

Let's have a brief idea of all the roles played when a chargeback if filed and is acted upon.

The Customer

The customer is usually the cardholder who has made a purchase. For our discussion, we will also regard a person who is seeing a transaction on his statement from a particular merchant, as a customer. In further discussions, we will be using terms ‘customer’ and ‘cardholder’ interchangeably. Credit card companies usually guarantee zero-fraud liability to their cardholders.

Issuing Bank

Issuing bank or the issuer is the provider of payment cards (credit, debit, prepaid, etc.) to customers. The issuer is the one responsible in regards to the payout of funds from cardholder to anyone. Also, it is obvious that the customer’s balance and authorization is managed by the issuing bank’s processor.

Issuing Bank Processor

The issuing bank processor manages data and transactions related to customer’s account.

Card Network

Visa, MasterCard, American Express, and Discover are the four major card networks. Card Networks literally provide network for payments. Following functions of Card Networks will give you a better picture:

- These take care of payments that take place.

- These manage settlement process between issuing and acquiring banks.

- These provide data connection and regulate flowing of funds between customer and merchant.

Acquiring Bank

Acquiring Bank is the financial body behind Card Networks. Their main function is to receive funds through card network on the merchant’s behalf from customer’s issuing bank.

Merchant Account Processor

The merchant account processor is a company that partners with an acquiring bank to process payments on behalf of the merchant. Merchants typically have a closer relationship with their account processor than their acquiring bank. A merchant’s processor and acquiring bank can be, and often are, the same institution.

Merchant Commercial Bank Account

Merchant commercial bank account is where the funds are deposited after the acquiring bank acquires those from the issuing bank through card network. This is the last stop of funds transferred from a cardholder.

Also, when a chargeback is initiated, the funds from this account are automatically withdrawn to get them moved back to cardholder’s account.

Payment Gateway

The payment gateway does the complex work of building secure connections to merchant account processors. It acts as a “virtual” credit card terminal allows a merchant to submit payments to a processor via the internet. It is often analogized as a virtual credit card terminal. Payment gateways also provide fraud filters, recurring billing payments, and other valuable functionalities to assist ecommerce companies.

The Merchant

Merchant is any business, company, brand, service provider, or other relevant party who provides a good or service in exchange for payment.

Possible Outcomes of a Chargeback

To identify the reason because of which an issuer files a chargeback, reasons codes were put into place. These reason codes are predefined and vary as per the credit card company. This list gives details about the chargeback reason codes.

If we categorize the outcomes of chargebacks, then you will observe that, every chargeback has three possible outcomes.

- Actual Fraud

- Chargeback/Friendly Fraud

- Product/Service Issues

Every chargeback, when filed, is either coded under a fraud reason code or a non-fraud reason code. But sometimes, when chargebacks are coded as fraud, they come out to be non-fraud after further investigations. And in such cases, chargeback fraud or friendly fraud is found to be the reason.

Because of this pseudo categorization of chargebacks into frauds, many merchants simple give in and assume those to be un-winnable cases of fraud. When studies rolled out, it was revealed that more than three quarters of chargebacks are just the cases of friendly fraud.

The Cost of Chargebacks

Accepting credit card payments is beneficial to a business and with chargebacks, we study how it may backfire. When a customer files a chargeback, no matter what reason there is behind it, you have to go through the whole process. It is time-consuming and holds your resources. This may result in a kickback for your sales too. Also, all the fees involved, the stringent process and complex procedures, who knows if all this is worth it in the end!

Online credit card transactions are regarded as ‘Card Not Present’ or CNP transactions. A merchant account agreement usually, specifies that the merchant is 100% liable for any type of mishaps that could take place.

During physical transactions, where both the cardholder and the card are present, it is the credit card institutions who take sole responsibility in cases of chargebacks. However, during online CNP transactions, merchants are solely responsible.

Unfortunately, there is no way out for a merchant in any of the two cases- actually fraud or a malicious attempt by the cardholder. And, if merchant fails to provide enough proof to back up the transaction, he has to face the consequences. Moreover, shipping charges involved to ship the products also go down the drain.

Credit card institutions usually favor cardholder’s concerns and focus on keeping them happy. This is simply because they want their customers to keep going back to them (and not lose their clientele) so that customers keep using their cards to make purchases. These institutions value their cardholders' best interests, such that any form of dissatisfaction or complaint usually results in chargebacks - all at the expense of honest merchants.

Chargebacks are not only responsible for bringing losses in financial aspects. Multiple chargebacks filed against single merchant has even worse consequences on the part of the merchant.

Following are some of the consequences that a merchant may have to face after multiple cases of chargebacks against him

- The credit card instituition may blacklist the merchant.

- The merchant’s online account may get terminated.

- Multiple chargebacks potentially ruin the reputation of an online store.

- Sales drop because merchants have to manage various procedures related to chargebacks.

Accepting Responsibility on Both Sides

Awareness about chargebacks is a must on both the sides- merchant’s as well as consumer’s. It is responsibility of both of them to accept consequences for the actions involved in the process.

Merchants’ Responsibilities

Merchants should take care that they are eliminating the risk of chargebacks, both legitimate and illegitimate. This can be done by,

- Offering attentive customer service.

- Providing high quality products and services.

- Keeping proper return and refund policies in place.

- Attending to transaction details. (this can drastically decrease friendly fraud)

By taking the necessary steps to detect fraud, merchants can identify transactions that could potentially lead to chargebacks. Preventing these fraudsters from making purchases reduces the risk of a resulting chargeback.

Preventing chargebacks is a way to go. But sometimes these are inevitable and the only thing merchants should resort to- Fighting chargebacks.

When more and more merchants dispute over false claims byt cardholders, banks become aware. This can go a long way in getting false chargebacks filed in future. It also helps educate consumers about what is a chargeback and when it should safely be used.

Cardholders’ Responsibilities

Cardholders have to be aware of one fact- Holding a card is a privilege and, not a right. This privilege comes with its own set and responsibilities and understanding how chargebacks work, is one of them.

Consumers should file a chargeback only in truly dire situations. They are the last resort, not the first action to take when seeking a refund. Consumers can’t impose chargebacks carelessly as this is harms merchants on more than one scales.

Hopefully, with proper education about what a chargeback is, both merchants and consumers can see a decline in the number of faulty chargeback claims.

{kind=link}